All employers in the UK must by law offer a workplace pension scheme and make contributions to the employee’s pension if they are eligible for automatic enrolment.

Once you have enrolled the employee into your workplace pension scheme, you must:

- Pay the minimum contributions to the pension scheme on time

- Let the employee leave the pension scheme if they ask to

- Let the employee re-join the scheme at least once a year if they’ve opted out

- Enrol the employee back in once every three years if they have opted out and if they are still eligible for automatic enrolment

Do we have to match an employee’s pension contribution?

The minimum contributions that an employer must pay into an employee’s staff pension scheme is a total contribution of 8% with at least a 3% employer contribution.

Image: www.thepensionsregulator.gov.uk

An employer can choose to pay more into an employee’s workplace pension than the minimum required. This also means that the employee can choose to reduce their own contributions. But the overall contribution must meet at least the minimum level set out by the government. The employee can also choose to increase their contribution.

Here are some examples of the different contribution categories that an employer could select when setting up their pension scheme:

Set 1: contributions calculated on gross earnings

Contributions based on gross earnings. They don’t include bonuses, overtime, commission, or certain staff allowances (such as shift pay or relocation allowance) in the calculation.

| Date effective | Employer minimum contribution | Staff contribution | Total minimum contribution |

| 6 April 2019 onwards | 4% | 5% | 9% |

Set 2: contributions calculated on gross earnings based on at least 85% of total earnings

These don’t include bonuses, overtime, commission, or certain staff allowances (such as shift pay or relocation allowance) in the calculation.

| Date effective | Employer minimum contribution | Staff contribution | Total minimum contribution |

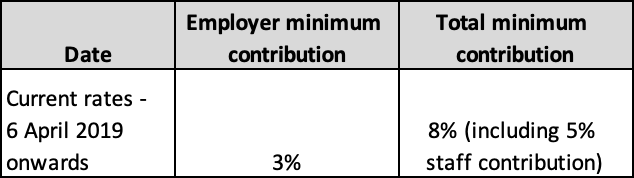

| 6 April 2019 onwards | 3% | 5% | 8% |

Set 3: contributions calculated on all earnings

Contributions based on all elements of staff pay and all earnings.

| Date effective | Employer minimum contribution | Staff contribution | Total minimum contribution |

| 6 April 2019 onwards | 3% | 4% | 7% |

Qualifying Earnings:

Pensionable earnings are between £6,032 and £46,350 per annum (£503 and £3,863 a month). Qualifying earnings include all payments, salary, overtime, commission, bonus, car allowance, etc. Employer contributions are 3% and Employee contributions 5%.

Tax relief and your workplace pension

To help employees save for retirement, the UK government usually provides tax relief on the contributions they pay into their pension savings. Tax relief is available on employee’s pension savings up to a standard limit known as the annual allowance, but their exact annual allowance depends on how much they earn.

Employers need to check that they’ve applied the same tax relief settings to their employees’ pension contributions on their payroll and on your pension scheme.

We would advise all employers to talk to their employees about their workplace pension and take the time to explain how much they will contribute. It is also worth pointing out that the more they contribute to their workplace pension plan, the more the taxman may provide in tax relief, subject to government limits.

Pensions are a complex subject and Paul Beare Limited can provide further information and support as part of our UK based HR offering. Information can also be found at www.thepensionsregulator.gov.uk.